Slowing Job Market Prompts Half-Point Rate Cut from Fed

Efforts to keep the labor market humming may also drive yields lower on cash equivalents, highlighting changing dynamics in the fixed-income market.

Key Takeaways

After keeping rates at a 23-year high for 14 months, the Fed lowered its short-term interest rate target by a larger-than-expected half-percentage point.

As inflation continued to moderate, yet still not to the 2% target, job market weakness took center stage and prompted the Fed to ease.

Fed rate cuts typically lead to lower yields on Treasury bills and popular savings vehicles, bringing reinvestment risk into focus.

As widely expected, the Federal Reserve (Fed) on September 18 cut the federal funds rate target for the first time since early 2020. The action marks the Fed’s first move since July 2023, when it lifted the target to a 23-year high. It finally puts the Fed on the same easing course as central banks in Europe, Canada and the U.K.

In addition to stimulating economic activity, Fed rate cuts also typically drive down lending rates and yields on cash-equivalent accounts and many bonds. Accordingly, loan rates may become more attractive, while savings and other cash-equivalent accounts may pay lower yields. We believe this scenario highlights timely opportunities in fixed income.

The Fed’s Focus Shifts

Fed officials turned their attention from inflation, which has slowed but hasn’t yet reached 2%, to employment. A series of recent reports painted the job market as weaker than originally thought. Policymakers hope their easing will provide a boost to the economy without jeopardizing inflation’s progress and the revered soft-landing economic outlook.

The half-point cut — larger than the quarter-point cut many had expected — dropped the short-term lending rate to 4.75% to 5%. Fed Board Chair Jerome Powell indicated the larger rate cut represented a “recalibration” of monetary policy as risks to inflation and employment become more balanced. He noted the cut aims to prevent further labor market weakness while maintaining the economy’s resilience.

Powell said he still views the current interest rate range as “restrictive” but expects to gradually restore policy to a neutral state. He characterized the half-point cut as “strong” and a sign of the Fed’s commitment to remain proactive.

The Fed also released its quarterly economic forecast showing policymakers expect a jobless rate of 4.4% by year-end, up from the 4% they projected in June. They expect the annual core inflation rate (personal consumption expenditures index) to land at 2.6% by year-end, lower than the 2.8% they forecasted in June. The latest projections also indicate Fed officials expect their short-term interest rate target to drop to a range of 3.25% to 3.5% by the end of 2025.

The Fed’s Employment Mandate Regains Prominence

The Fed’s inflation mandate drove central bank policy for more than two years. As prices soared to multidecade highs, the Fed pursued an aggressive tightening strategy that drove interest rates 5 percentage points higher over a 10-month period. During that timeframe, the other component of the Fed’s dual directive — maintaining stable employment — remained relatively healthy and garnered little Fed attention.

But, as we’ve noted since 2022, it takes time for Fed policy to work through and slow down the economy. We’ve already seen slowdown signs in the manufacturing and housing sectors and various consumer and inflation metrics. We’re now seeing the effects in the job market, where the unemployment rate has edged up this year, from 3.7% in January to 4.2% in August.

Additionally, the government has consistently revised downward key monthly and yearly job market figures. In August, the Bureau of Labor Statistics indicated it overstated by 818,000 the number of jobs created in the 12-month period ending in March. Furthermore, the agency has revised downward nearly every monthly job report for the last 18 months, as Figure 1 illustrates.

Figure 1 | Job Market Wasn’t As Strong As It Originally Appeared

Non-Farm Payroll Employment: Revisions Between Monthly Estimates, Seasonally Adjusted

Date | First Estimate | Final Estimate | Change |

January 2023 | 517,000 | 472,000 | -45,000 |

February 2023 | 311,000 | 248,000 | -63,000 |

March 2023 | 236,000 | 217,000 | -19,000 |

April 2023 | 253,000 | 217,000 | -36,000 |

May 2023 | 339,000 | 281,000 | -58,000 |

June 2023 | 209.000 | 105,000 | -104,000 |

July 2023 | 187,000 | 236,000 | +49,000 |

August 2023 | 187,000 | 165,000 | -22,000 |

September 2023 | 336,000 | 262,000 | -74,000 |

October 2023 | 150,000 | 105,000 | -45,000 |

November 2023 | 199,000 | 182,000 | -17,000 |

December 2023 | 216,000 | 290,000 | +74,000 |

January 2024 | 353,000 | 256,000 | -97,000 |

February 2024 | 275,000 | 236,000 | -39,000 |

March 2024 | 303,000 | 310,000 | +7,000 |

April 2024 | 175,000 | 108,000 | -67,000 |

May 2024 | 272,000 | 216,000 | -56,000 |

June 2024 | 206,000 | 118,000 | -88,000 |

July 2024 | 114,000 | 89,000* | -25,000 |

Data as of 9/6/2024. Source: U.S. Bureau of Labor Statistics. *Represents the second estimate for July 2024; the final estimate was unavailable as of 9/18/2024.

Consumers to Feel the Impacts of Lower Rates

With the Fed now in easing mode, American savers and investors can expect to feel the effects. Cuts to the Fed’s rate target typically filter through to consumer lending rates, including mortgages and other loans. Accordingly, it’s possible prospective homebuyers may see some modest near-term relief in mortgage rates.

Fed rate cuts also affect CDs, various savings accounts and shorter-maturity bonds. This means the current yields on cash-equivalent holdings may downshift in the coming weeks.

We believe this dynamic underscores a time-sensitive consideration in some fixed-income portfolios: reinvestment risk. It also highlights potential opportunities in the bond market.

Confronting Reinvestment Risk

Reinvestment risk is the possibility that investors may be unable to reinvest cash flows at the same yield they’re currently earning. This risk typically emerges when interest rates are falling, presenting a two-pronged challenge for some fixed-income portfolios:

Rates on Treasury bills, savings accounts, CDs and other cash equivalents typically move in tandem with the federal funds rate. So, when the Fed cuts short-term rates, yields on these holdings also drop, reducing investors’ monthly income.

A declining interest rate environment generally drives bond prices higher, pushing up the cost of reinvesting cash into securities with longer maturities and higher yields.

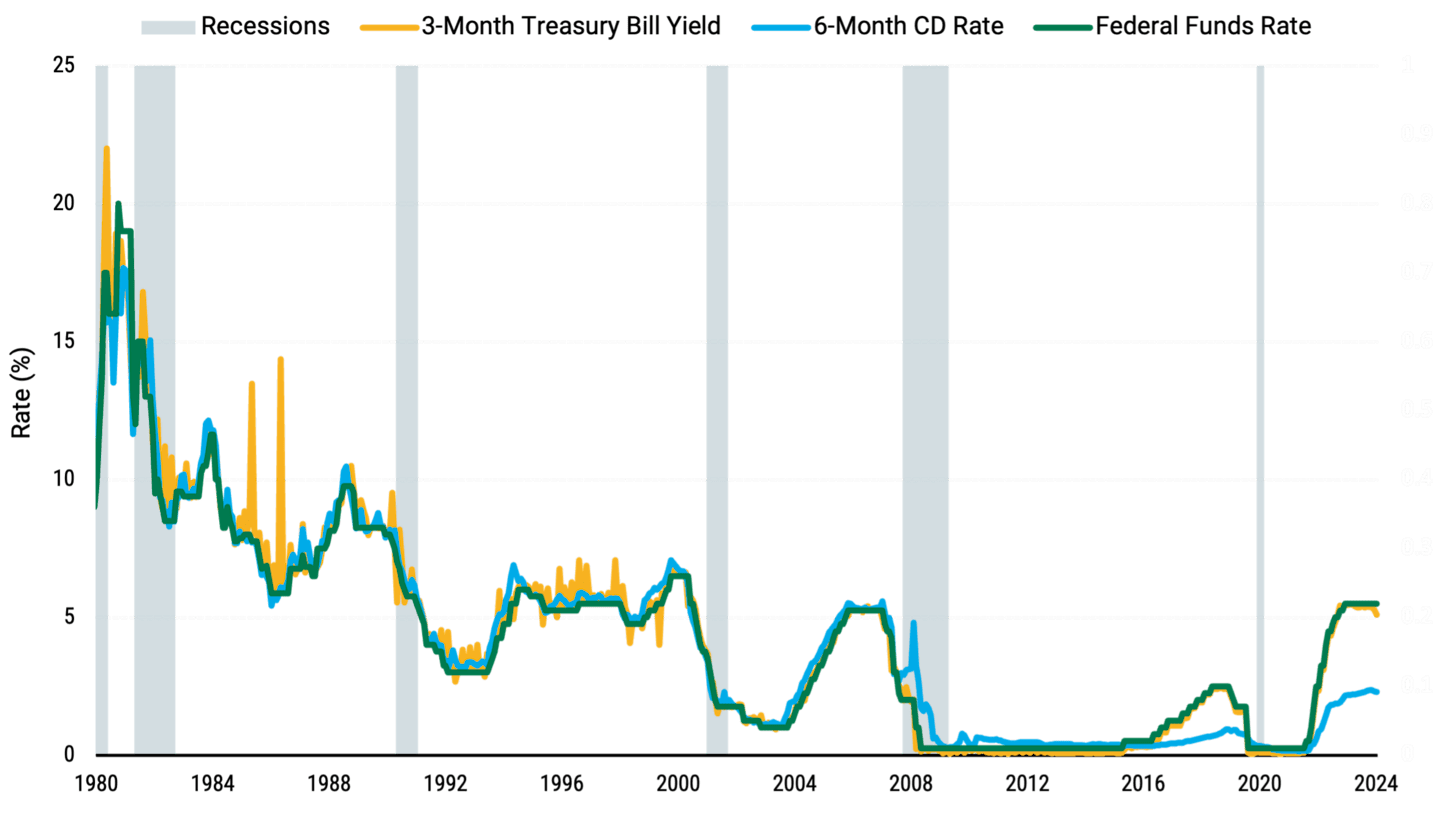

We expect yields on Treasury bills, CDs and similar products to follow history (see Figure 2) and track the Fed’s target rate lower. Therefore, reinvesting in these same vehicles won’t provide the income potential they offer today. And as the Fed continues to ease, shifting into longer-maturity fixed-income securities may get more expensive.

Figure 2 | Short-Maturity Yields Have Tracked the Fed Funds Rate

Data from 8/31/1980 - 8/31/2024. Source: FactSet. Past performance is no guarantee of future results.

In our view, there still is time to confront reinvestment risk. Waiting until rates decline further to shift into higher-yielding, longer-maturity bonds could mean buying those securities at higher prices. But making the move before the Fed makes additional rate cuts may help by:

Securing the relatively higher yields still available today.

Adding duration, which can generate capital appreciation when interest rates fall.

We believe higher-quality bonds with potentially attractive yields may help weather a dovish Fed and a slower economy. Such securities include U.S. Treasuries and higher-credit-quality corporate and securitized bonds.

Author

Past performance is no guarantee of future results. Investment returns will fluctuate and it is possible to lose money.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments' portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

In certain interest rate environments, such as when real interest rates are rising faster than nominal interest rates, inflation-protected securities with similar durations may experience greater losses than other fixed income securities. Interest payments on inflation-protected debt securities will fluctuate as the principal and/or interest is adjusted for inflation and can be unpredictable.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

Diversification does not assure a profit nor does it protect against loss of principal.