5 Questions About Investing in Small-Cap Stocks for 2024

We take a look at investing in small-cap stocks during an eventful and unpredictable year in the stock market.

Key Takeaways

The stock market was volatile in August, bolstering our view that an economic slowdown is ahead.

We believe that small-cap stocks have largely priced in a downturn.

We also think small-cap stocks trade at discounted valuations, but inflation still poses a risk.

We opened 2024 with some optimism for small-cap stocks after facing turbulence the year before. We thought small-caps had a compelling outlook, given their inexpensive valuations and structural benefits to the asset class, like reshored manufacturing and supply chains.

Unfortunately, much of the first half of 2024 proved challenging for small-caps as continued enthusiasm for artificial intelligence (AI) led to increasing market concentration and exuberance for large-cap growth stocks. But July marked the beginning of a market rotation that may favor small-caps as investors question capital expenditures and return on investment in AI.

The broadening of the market and the prospect for rate cuts during the rest of 2024 may serve as tailwinds for small-caps. In addition, small-cap earnings growth is expected to outpace large-caps as we head into 2025. With that in mind, we’ve honed our outlook for the asset class.

1. How can small-cap stocks outperform in a recessionary environment if one materialized in 2024?

Small-cap companies tend to underperform in the first half of a recession. But a recession hasn’t emerged this year and the market has proved to be more resilient than expected. For much of the year, consumer spending has remained strong, and the labor market has been sturdy.

However, there are renewed concerns about the strength of the U.S. economy and the incredible resilience of the U.S. consumer. A weaker-than-expected July jobs report, showing unemployment inching up to 4.3%, triggered a one-day market rout and renewed chatter about an impending recession.1 There are signs that consumers are pulling back on their spending, which could make the critical leg that supports the U.S. economy wobbly.

We believe that an economic slowdown is coming but remain skeptical about the prospects of a hard landing. As the economy slows, we would expect a gradual rise in unemployment and jobless claims. However, a spike in these measures could be cause for concern.

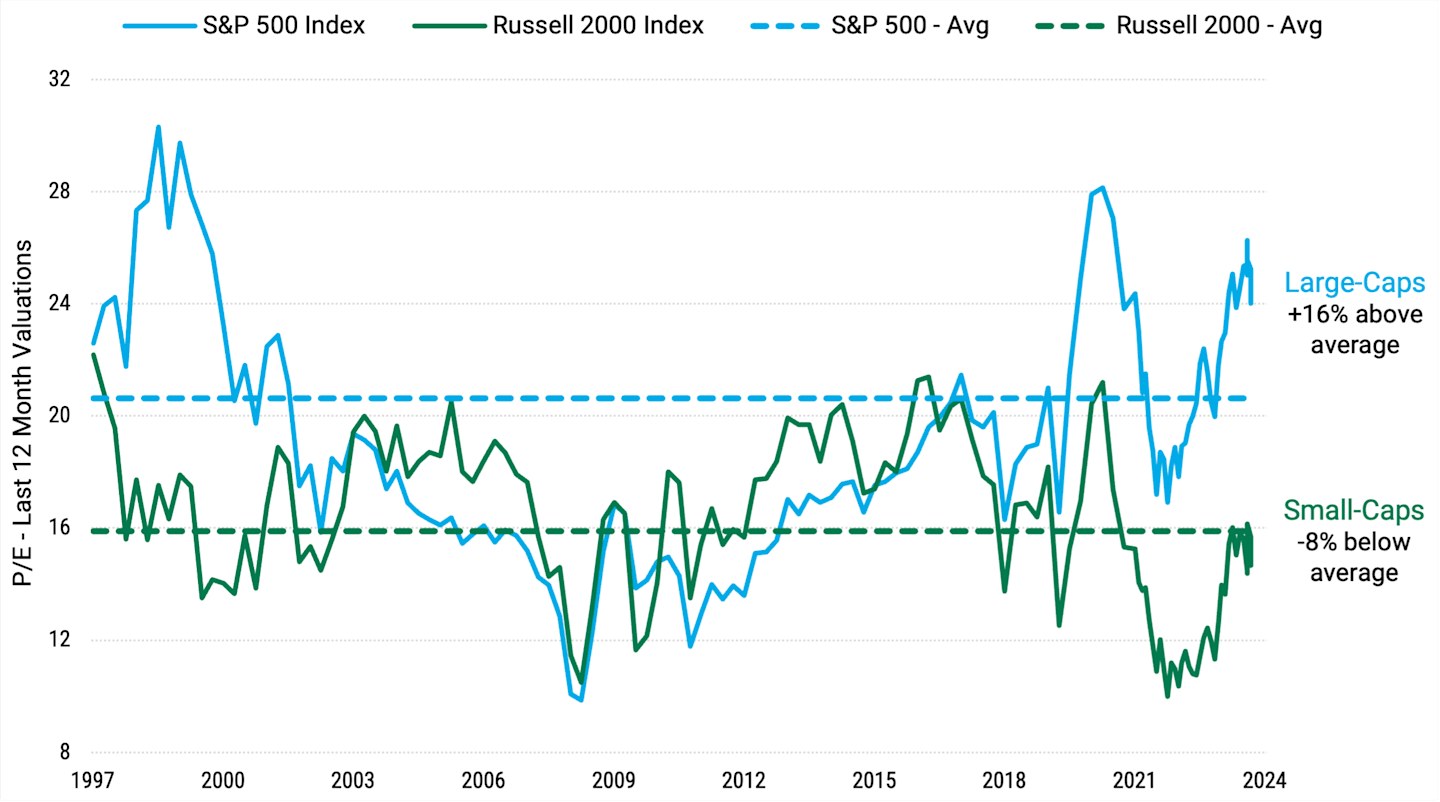

Whether a recession occurs in late 2024 or into 2025 remains to be seen, but we believe small-cap investors have largely priced in a downturn. After the market sell-off in early August, small-caps, as measured by the Russell 2000® Index, were trading approximately 8% below the 20-year average, as shown in Figure 1, while large-caps, as measured by the S&P 500® Index, traded at 16% above the 20-year average.2

Figure 1 | Value Disparities Between Large- and Small-Cap Stocks

Data from 12/31/1997 – 8/6/2024. Source: FactSet. Past performance is no guarantee of future results. Price to Earnings Ratio (P/E) is defined here.

2. Over one-quarter of small-cap companies are losing money today. Is this a risk to small-cap stocks?

It remains true that about 27% of small-cap stocks don’t make a profit, and roughly one-third of these unprofitable companies are biotechnology or pharmaceutical companies.

Small-cap biopharma firms aren’t generally designed to generate revenue or profits while developing new drugs and therapies. If their products are proven effective, Big Pharma companies often acquire them. Given the pipeline of new drugs under development, we think small-cap biopharma presents potential opportunities in the market.

Outside of biopharma, the remaining unprofitable small-cap companies risk bankruptcy if the economy experiences a hard landing or interest rates stay high. There has been a significant increase in bankruptcy filings this year. Notable consumer companies like Conn’s and Big Lots are on the skids and facing the prospect of bankruptcy. Formerly high-flying software company 2U filed for Chapter 11 protection in July.

Higher interest rates pose a risk for small-cap companies with more leverage, as a large amount of debt will come due in the next two years. Lower rates would help alleviate the refinancing risk.

Active managers can help identify small-cap companies with financial characteristics that can withstand economic turbulence and don’t rely on lower rates to survive while avoiding those that do.

3. Companies choosing to stay private longer has resulted in fewer publicly traded investment options for small-cap managers. Is this a drawback for small-cap stocks?

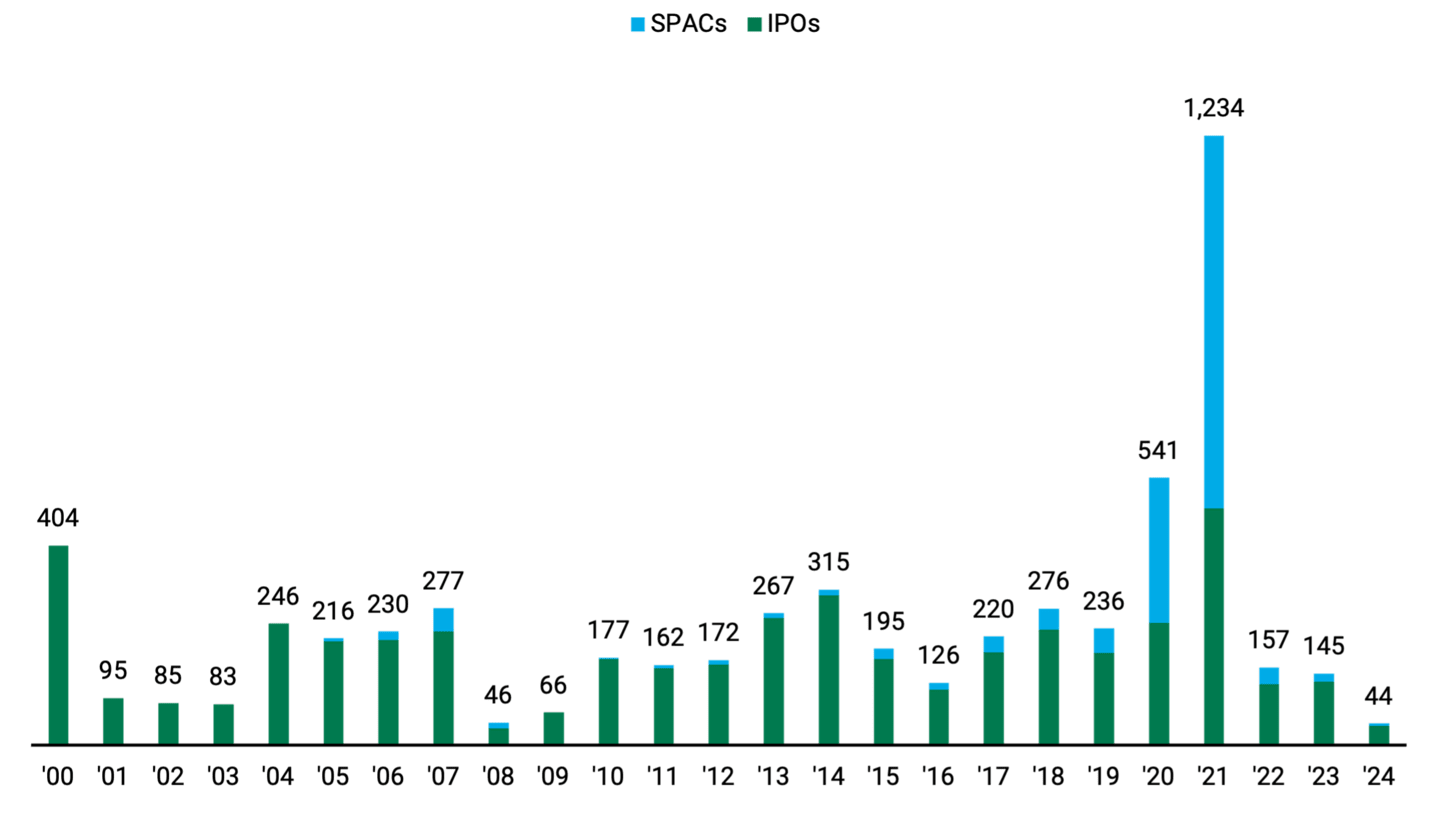

After a surge of initial public offerings (IPOs) in 2021 — driven mainly by special purpose acquisition companies (SPACs), which are public companies created to buy or merge with a private enterprise — the number of IPOs dwindled in 2022 and 2023, as shown in Figure 2.3 While a boom in private investing has encouraged companies to stay private longer, we believe there are signs that IPO activity is picking up.

Figure 2 | IPO Activity Has Dwindled Since 2021

Data from 1/1/2020 – 4/30/2024. Source: FactSet, Jefferies.

We’ve seen several companies we deem high quality go public in 2024, including social news and forum platform Reddit. Another notable IPO was Astera Labs, whose shares went up 72% on the first day of trading in March. To be fair, an IPO doesn’t ensure an increase in share prices; some offerings fare poorly in initial trading.

While the spike in volatility in August isn’t likely to help the IPO calendar, we expect an increase in deals in 2025. If more companies go public and participate in the initial outperformance, we think an uptick in IPO activity could help small-caps by increasing interest in the asset class. We also think it may have appeal to institutional investors looking to unlock money they have tied up in private equity or venture capital if companies go public.

4. Regional banks occupy a big space in the small-cap universe. Do regional banks pose a risk for small-caps?

On the surface, regional banks looked shaky early in 2024. The still-inverted yield curve continued to apply pressure to net interest margins. When New York Community Bank unexpectedly took an unexpectedly large charge and raised capital to increase its loan loss reserve, many investors had déjà vu of March 2023, when several regional banks went under.

At the time, we believed that New York Community Bank had unique problems and that most regional banks were in relatively good shape despite headwinds from multiple sources.

While many small-cap managers lacked confidence in regional banks, our conviction held up, and we maintained an overweight position. We believe regional bank valuations are attractive, and we analyze the industry to find banks we believe have strong management teams, sound financial characteristics, above-average loan loss reserves, and those without high exposures to risky areas in commercial real estate.

With interest rates likely to decline, we believe our conviction in regional banks may be rewarded. July 2024 illustrated the pent-up demand and potential upside for banks as inflation cooled and the yield curve steepened. The group, as measured by the KBW Regional Bank Index (KRX), was up approximately 25% in a matter of weeks, well above the S&P 500 and the Russell 2000.4

5. What if inflation picks up again?

Inflation threatens our small-cap thesis. If inflation ticked up and pushed central banks to increase rates, it would spell trouble for many small-cap companies with higher debt levels.

While inflation remained stubbornly above the Federal Reserve’s (Fed’s) 2% target for much of the year, it has started cooling. The Fed appears poised to be on a path of reducing interest rates well into 2025, which could benefit small-cap companies. However, if the recent improvement in inflation stalls or reaccelerates, it would be difficult for small-caps to outperform large-caps.

Final Thoughts

We started 2024 with compelling reasons to consider investing in small-cap stocks. We continue to believe small-caps are attractive, given their valuations, accelerating earnings growth and years of underinvestment in the asset class.5

The July rotation, in which small-caps beat large-caps by approximately 10%, illustrates the potential for the asset class to outperform as dollars flow from groups that have performed well, like big-cap tech, to areas that have lagged, like small-caps.6

While inflation and recession fears could derail small-caps in the near term, we believe potential bad outcomes have largely been priced in, and the outlook is improving for this long-forgotten asset class.

Authors

Senior Investment Director

Explore Our Small-Cap Capabilities

U.S. Bureau of Labor Statistics, “The Employment Situation ̶ July 2024,” News Release, August 2, 2024.

FactSet, as of August 6, 2024.

SPACs are investment vehicles formed to acquire a private company and make it public. The boom in SPACs ultimately led to only a handful of new publicly traded small-cap companies, and approximately 40% were liquidated by the end of 2023.

The KBW Regional Banking Index seeks to reflect the performance of U.S. companies that do business as regional banks or thrifts.

Based on measures of tangible book value per share and price-to-earnings ratio.

Source: FactSet. Based on the performance Index A and Index B during the month ending 7/31/2024.

Historically, small- and/or mid-cap stocks have been more volatile than the stock of larger, more-established companies. Smaller companies may have limited resources, product lines and markets, and their securities may trade less frequently and in more limited volumes than the securities of larger companies.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments' portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.