Will the Fed's Rate Cut Be a Boon for Small-Cap Stocks?

Explore how rate cuts can potentially boost small-cap stocks, and why this asset class may be poised for a resurgence.

Key Takeaways

Rate cuts have historically benefited equities, particularly small-caps.

On average, smaller companies have historically outperformed large companies by nearly 5% one year after a rate cut.

Why? Rate cuts spur economic growth and reduce the cost of capital, which is particularly helpful to small companies.

Seven? Three? Zero? The expectation for the number of rate cuts in 2024 has bounced around throughout the year, but the direction hasn’t. Rates are expected to go down. The next Fed action will likely be a cut, whether inflation continues to moderate toward the 2% target or the economy materially slows.

Could a rate cut help beleaguered small-cap stocks? We think so.

Why Have Small-Caps Underperformed?

Small-caps have been mired in what may be the longest period of underperformance versus large-caps in history, with the interest rate environment one of many challenges.

After the Great Financial Crisis, near-zero rates were a headwind for small-caps, as economic growth was sluggish and inflation was non-existent, bordering on deflation. Small-caps' economic sensitivity, combined with higher exposure to “spread businesses” like banks (which thrive on a steeper yield curve), represented a double whammy for small-caps versus large-caps during this period.

More recently, the multi-year inverted yield curve has been a problem for smaller companies, pressuring earnings and predicting an impending recession. We believe Investors have been waiting for the yield curve to steepen before increasing their allocations to the asset class.

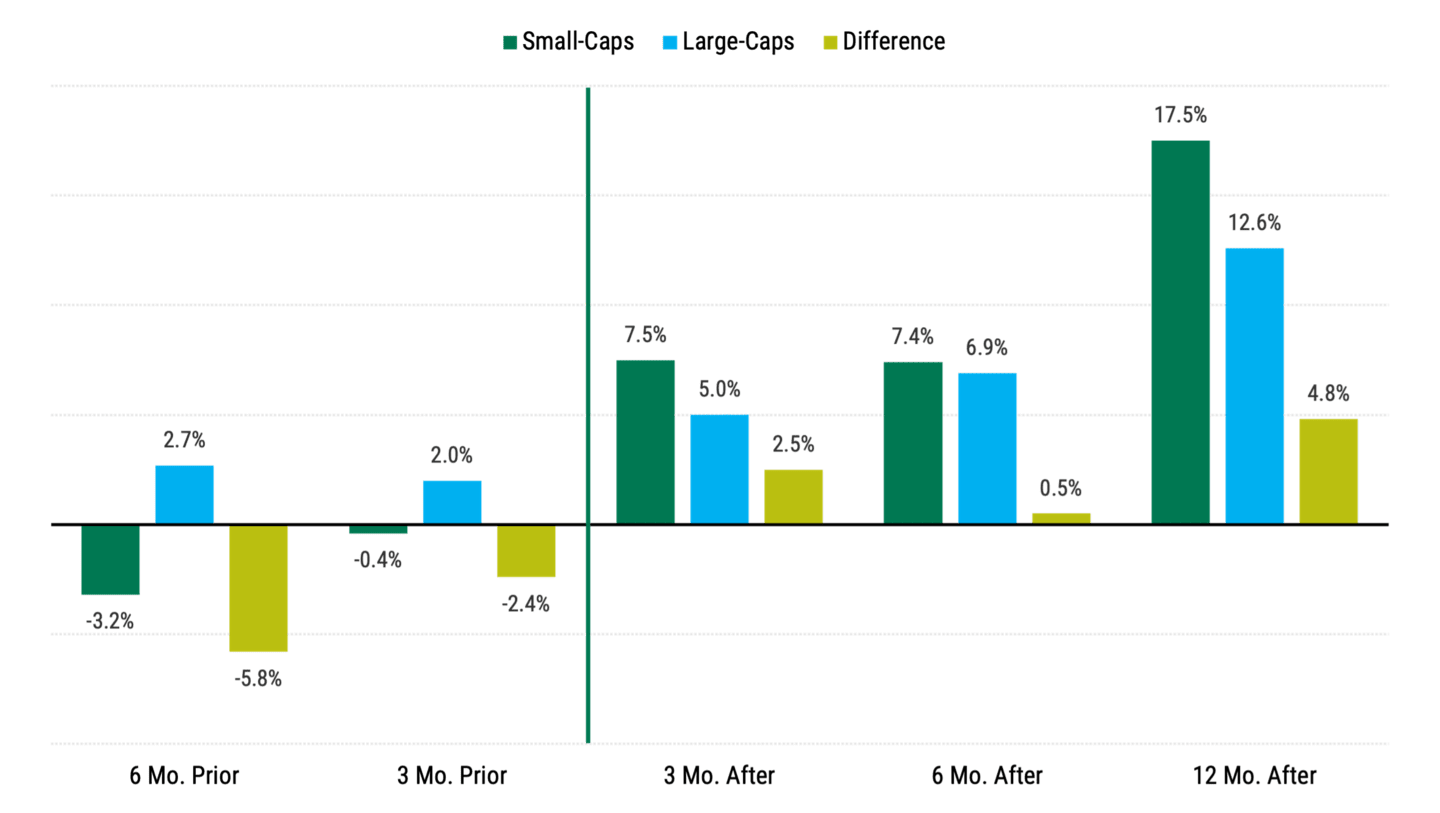

This phenomenon isn’t new. Historically, large-caps have outperformed their small-cap counterparts heading into a rate cut. See Figure 1.

What Does a Rate Cut Mean for Small-Cap Stocks?

Rate cuts have represented a positive catalyst for markets, particularly for small-caps. As we see in Figure 1, smaller companies have historically outperformed large companies by nearly 5% on average a year after a rate cut.

Figure 1 | Small-Caps vs. Large-Caps Before and After Rate Cuts

Data from 5/1/1980 – 3/31/2022 (12 months after the last rate cut). Source: FactSet. Small-cap stocks and large-cap stocks are represented by the Russell 2000® Index and the Russell 1000® Index, respectively. Past performance is no guarantee of future results.

In addition to potentially spurring economic growth and benefiting interest-rate-sensitive businesses, rate cuts can also lower the cost of capital for many small-cap companies, where debt service represents a more material impact on profitability than for large-caps.

We think rate cuts have the potential to improve growth and profitability and reignite interest in the forgotten small-cap asset class.

Author

Historically, small- and/or mid-cap stocks have been more volatile than the stock of larger, more-established companies. Smaller companies may have limited resources, product lines and markets, and their securities may trade less frequently and in more limited volumes than the securities of larger companies.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments' portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and are subject to change without notice.